10th October 2024

Download the report as a PDF (0.6Mb)

Introduction

HM Revenue and Customs (HMRC) is at the heart of the UK’s financial stability. As the Government department responsible for administering the tax regime and collecting revenues due to the Exchequer, its role has never been more critical.

This report examines the state of HMRC in the 2023-24 tax year, focusing on revenues, resources and compliance, as well as the challenges it faces in an increasingly complex tax system.

The main findings of the report are:

- Though HMRC has kept the tax gap around 5% for years, the sheer volume of uncollected tax, compounded by increasing taxpayer complexity, underscores the urgency for more robust enforcement. In the latest data available (2022-23) the tax gap stands at £39.8 billion. Compounding this is a staggering £38 billion in outstanding debt by March 2024, a persistent burden on public finances.

- HMRC continues to face fierce criticism over customer service failures, particularly around its telephone services, where response times and satisfaction levels have plummeted. Staffing shortages, falling expertise, and retention issues—especially among frontline roles—only exacerbate these weaknesses.

- Whilst compliance activities yielded significant amounts of tax that would otherwise be lost to HM Treasury, HMRC are making basic mistakes in cases which have cost considerable amounts of lost revenue.

While HMRC’s importance to the UK economy is unquestionable, it is under intense pressure to modernize, close compliance gaps, and vastly improve its service delivery if it is to meet the mounting demands of an increasingly complex tax system.

1. Tax revenues

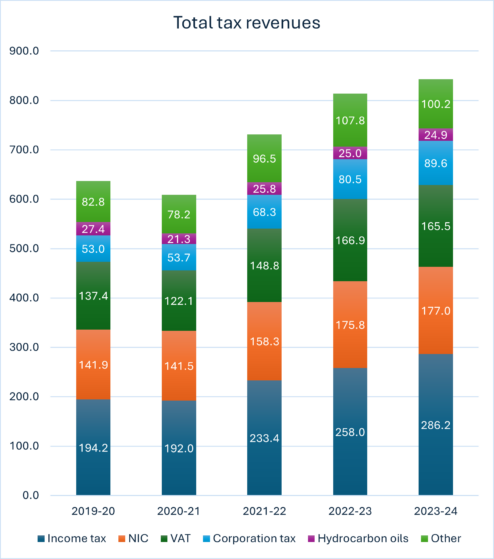

Total tax revenues continue to increase year on year, with total tax revenues of £843.4 billion in 2023-24, a 3.6% increase from the previous year. The largest revenue raisers are Income Tax, National Insurance Contributions (NIC) and VAT, which combined consistently account for three quarters (74.5% in 2023-24) of total tax revenues.

Figure 1, Total tax revenues

The increase in tax revenues is due to a number of economic factors, such as wage growth and inflation, as well ‘fiscal drag’ as frozen tax thresholds draw more people into the tax net and increase the numbers paying at higher rates. This trend is projected to increase further in the coming years. In 2021-22, there were 33 million income taxpayers. This is projected to increase to 37.4 million in 2024-25[1].

1.1. The tax gap and debt balance

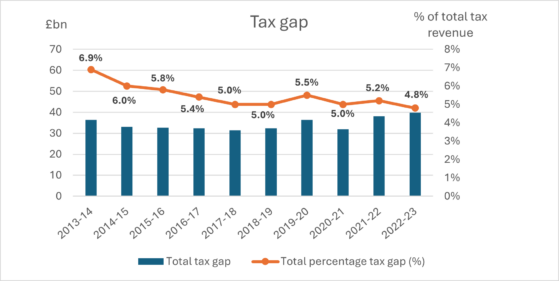

The tax gap is a measure of the taxes collected by HMRC compared to the theoretical liability, which should be collectable.

HMRC are tasked with holding the tax gap down below 5% in proportionate terms, but the amounts in cash terms continue to grow as fiscal drag continues to increase the ‘tax base’. The tax gap has remained around 5% over recent years, down from a high of 6.9% in 2013-14. The figure for 2022-23 is 4.8%, or £39.8 billion. However, it should be noted that HMRC has a habit of adjusting figures for the prior year which means they can report the tax gap proportion ‘continues to fall’ The original figure for 2021-22 was below 5% but adjusted upwards following the release of the figures for 2022-23.

Figure 2, Tax gap

The tax gap is not a complete measure of compliance and collection across the tax system. HMRC don’t attempt to quantify the amounts lost to the UK Exchequer represented by profit shifting by multinational corporates under the current international tax rules. Nor have HMRC yet published a measure of the offshore tax gap – where those subject to UK taxation on assets held abroad have not declared their income and gains accurately. TaxWatch[2] continues to press the importance of the latter, and its concerning that this assessment is now so delayed given upcoming changes to the tax regime for non-UK domiciled individuals.

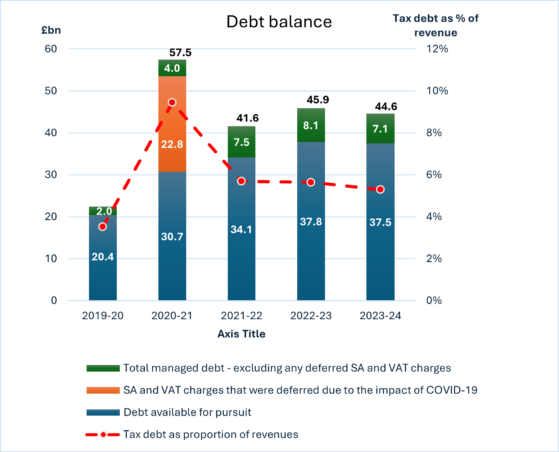

1.2. Debt balance

Even where the amounts of tax due by a UK taxpayer has been declared and assessed accurately, the revenues may still form part of the tax gap if the payment isn’t collected – this is known as the debt balance.

Debt in cash terms rose dramatically during Covid-19 under various ‘time to pay’ flexibilities offered to taxpayers who applied for easements in payment terms, especially for VAT. Significant amounts of aged debt have been written off as uncollectable, and yet the outstanding debt that HMRC accounts suggest is collectable as of 31 March 2024 remains high at £38 billion. At Spring Budget 2024[3] the debt management facility had to be extended to reflect increasing time lags between tax being due for payment, and the date it is actually received into the Exchequer, costing £3.4 billion over the five year period to 2027/28.

Figure 3, Debt balance

2. Financial resources

The cost of running HMRC continues to increase yearly, although the increase in 2023-24 is a below inflation 1.7% cash uplift on the previous year, its budget continues to rise in monetary terms, spending £5.5 billion in 2023-24.

2.1. Expenditure by directorates

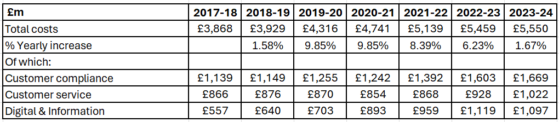

Table 1, Core expenditure by Directorate

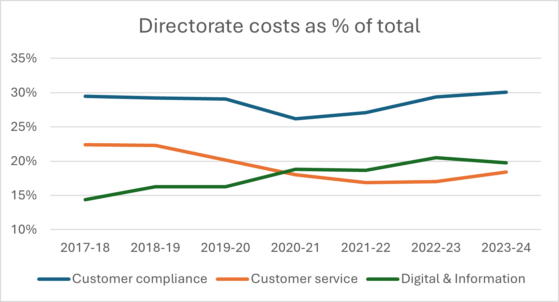

Whilst table 1 shows the variable budget increases over time (reflecting the sporadic additional resources awarded to the department to cope with events like Brexit and the Covid-19 pandemic), the composition has also substantially changed over the last seven years (figure 4). In 2017-18, Digital & Information accounted for less than 15% of the department budget. By 2024 this had doubled in cash terms, growing far quicker than compliance or customer services sections to now represent 20%, having overtaken customer services in 2020-21. The overall picture for customer compliance and customer services is bumpier, with a fall coinciding with the COVID pandemic and slight increases thereafter.

Figure 4, Directorate costs as percentage of total

3. Human resources

HMRC is the third largest Government Department in terms of staff numbers, after the Ministry of Justice and Department for Work and Pensions (DWP), with over 60,000 staff members.

3.1. Staff numbers[4]

The overall average number of FTE staff fell during the 2023-24 year by 1,059 following a significant increase in the previous year.

![]()

Table 2, HMRC staff numbers, FTE[5]

Prior to winning the July 2024 General Election the Labour Party committed to a significant increase in staff within HMRC as part of their pledge to close the tax gap. This commitment was re-stated at the end of July by the new Chancellor Rachel Reeves. Details of how these new officials, and the money to pay their salaries, will be genuinely additional, rather than replacing staff who have recently left, will hopefully be clarified in the Autumn Budget 2024.

3.1.1. Staff numbers by main directorates[6]

Table 3, HMRC staff numbers by main Directorate, FTE as of 31 March

The numbers of full time equivalent (FTE) staff in the Customer Services directorate have consistently fallen as HMRC moves towards digitising customer service as much as possible. In 2017-18, 40% of HMRC staff worked in Customer Services, but by 2023/24 this had fallen to 30%.[7]. Customer service is in a vicious circle where attrition rates of more experienced staff have led to an influx of temporary workers with inadequate training, leading to further slumps in morale.

The figure of 18,434 FTE staff as of 31 March 2024 does not include an additional 923 staff whom we understand are on temporary contracts, drafted in to address short term failings in HMRC’s duties to provide reasonable customer service. TaxWatch has previously reported[8] on how the use of low paid, relatively inexperienced staff to handle complex tax queries is not a good way of improving customer service levels. With increasing proportions of calls being more complex enquiries, more resources need to be spent on each call, with more escalation to senior staff. Just tracking staff numbers is rarely insightful into the satisfaction of the interactions. Data measuring satisfaction with the call handler is not collected for those cut off.

In contrast, the number of staff working specifically in compliance roles have increased, as HMRC have been tasked with raising more revenue. From 23,514 in 2017-18, the figure increased to a high of 28,699 in 2021-22, before modest falls in the last two years. Staff working in Customer Compliance accounted for 39.6% of total staff numbers in 2017, this increased to 44.7% in 2023-24.

The number of staff in Corporate Services has also increased each year since 2017-18, reaching 10,624 in 2023/24 from 6,827 six years ago, a very dramatic proportional increase from 11.5% in 2017/18 to now over 17%. Whilst there is a marked shift in emphasis within HMRC on downstream compliance, as opposed to customer service in their bid to digitise customer service interactions as much as possible, its less clear what factors have caused the large increase in Corporate Services.

3.1.2. Changes in staff composition

Recent years have seen changes in the composition of HMRC’s workforce. Whilst these changes are reflected more broadly across the Civil Service, they represent areas of concern for HMRC’s ability to recruit and retain the skilled and experienced workforce required to implement tax policy.

3.1.3. Falling number of ‘Tax Professionals’

There was a sharp fall in the number of Tax Professionals in 2018 and, although the number of has fluctuated in recent years, they remain far fewer than in 2017, despite the increase in staff working in customer compliance.

Table 4, Number and proportion of ‘tax professionals’ in HMRC

The reason for the sudden fall in FTE roles labelled ‘Tax Professional’ in 2018 is not clear. We can only assume that HMRC re-categorised many roles under different professions, or de-categorised them entirely.

The largest increases in the relevant years are in ‘counter fraud’, ‘digital, data and technology’ professions and those with no reported profession. The decision to re-categorise tax professionals makes it harder to gauge the levels of tax knowledge and expertise in HMRC and whether there has been a conscious decision by management to more accurately interpret the categories, or whether the fall in recent years is attributable to people within tax professional roles leaving HMRC and not being replaced.

That being said, the title of ‘Tax Professional’ is a term ascribed by management to the role, rather than the staff member occupying it at a given time. HMRC don’t keep records about the staff who hold external tax qualifications such as the ATT or CTA offered by the Chartered Institute of Taxation, nor whether tax professional roles are occupied by staff who have completed HMRC’s own internal tax training programme, the Tax Specialist Programme. The phrase Tax Professional is therefore a bit misleading.

3.1.4. Changing age profile

HMRC’s workforce has become more hour-glass shaped over time. In 2010, almost 70% (68%) of HMRC’s workforce was aged 40+. In 2024, this had fallen to 61%. Over this period the proportion of HMRC staff aged 40-49 fell from 34.3% to 22.7%. The age groups that increased (by around 5 percentage points respectively) were those aged 60+ and those aged 30-39. This suggests a ‘hollowing out’ of middle aged HMRC staff, with implications for knowledge transfer and progression within the department.

3.1.5. Inflated grades?

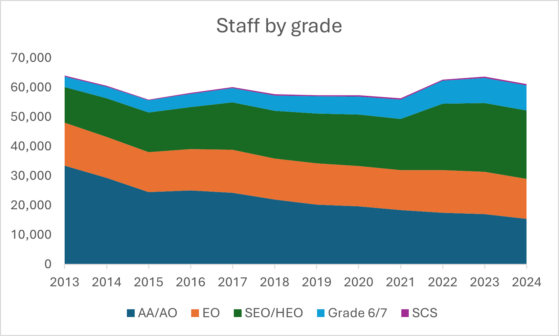

Over time, HMRC has witnessed a more extreme version of the civil service wide trend of ‘grade inflation’, which has shifted the seniority of the staff up the structure. With the phasing out of the most junior AA grade entirely, the number of AA/AO staff has dramatically fallen (from 33,514 in 2013 to 15,430 in 2023, down 54%), whilst the number of mid-tier grades (SEO/HEO and Grades 6 & 7) have almost doubled or more over the same period. The needs of the department have changed over time with automation and digitisation of services, reducing the need for clerical staff. As figure 5 demonstrates, the number of staff in higher grades, either SEO/HEO or Grade 6 and 7, have increased as a proportion of the workforce. The proportion of those in SEO/HEO roles has increased significantly since 2013, when only 18.7% occupied such roles. In 2024 this proportion had increased to 37.9%. There is a similar trend for those in Grade 6 and 7, with only 5.61% occupying these roles in 2013, compared to 13.9% in 2024.

Figure 5, Staff by grade

Key:

AA/AO = Administrative Assistant/Officer

EO = Executive Officer

SEO/HEO = Senior/Higher Executive Officer

SCS = Senior Civil Service level

Trends in workforce composition also suggest a degree of grade inflation, where roles have been re-categorised with lower requirements than had formerly been the case. Over the last 15 years pay and recruitment freezes, combined with older staff retiring, have meant that it is hard for HMRC to recruit like-for-like replacements. Grade inflation is an attempt to prevent staff from leaving by re-categorizing roles with lower requirements, meaning staff successfully securing those roles achieve promotion in salary terms before they would otherwise be ready, leading to those being promoted having less technical experience. The Institute for Government[9] have identified this as a potential problem which could stymie HMRC in the future, as roles become more blurred due to premature promotions, exacerbating existing problems of recruiting external applicants and undermining morale.

3.1.6. Entrants and leavers

As part of Labour’s commitment to increasing tax revenues collected, they have pledged to increase the staffing levels of HMRC. However, as recent years’ figures show, HMRC has a staff retention issue with an increasing proportion of the total workforce leaving each year.

Recruitment has fluctuated in recent years, 2021-22 saw a near doubling in recruitment, which has since markedly fallen, with only 3,564 new external recruits in 2023-24, and only 535 recruited from other departments, the lowest figure in recent times.

Table 5, HMRC FTE entrants per year

In contrast to the number of recruits, the number of staff leaving HMRC each year has increased in each of the last three years. In 2024, there were 5,154 leavers, including people who left HMRC for another governmental department, as well as those who resigned and retired. The annual turnover rate has increased to more than 8% in the last two years, meaning that around eight in 100 staff are leaving HMRC each year.

Staff turnover is an important indicator of staff satisfaction and has implications for technical skills and the costs of recruitment to replace personnel who have left. Turnover has increased over recent years.[10] In 2021 it was 3,363 (a rate of 5.8%), increasing to 5,154 (8.3%) in 2024. This indicates that HMRC may have a retention issue, posing a significant threat over the long term if this trend persists. Replacing staff is time and resource intensive and may have a wider impact on team morale if the turnover rate is high. It is also difficult to recruit the levels of expertise that are required for technical tax roles to replace the knowledge and experience that is being lost. It is worth noting that this is a problem across the whole Civil Service as identified by Institute for Government[11].

Table 6, HMRC FTE leavers per year

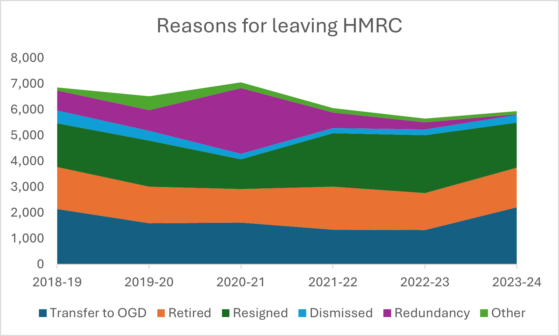

Civil service statistics provide a breakdown of the reasons for leaving HMRC. However, they are given in terms of headcount rather than FTE. Despite the differences in overall figures, the breakdown provides an interesting insight into why people leave HMRC. As figure 6 shows most leavers either move to another governmental department, resign or retire. The one exceptional year is 2020-21, during which a higher number of staff (2,550) were made redundant following the re-organisation of HMRC and closure of smaller office buildings.

Figure 6, Reasons for leaving HMRC

In 2024, those transferring to other departments, either on a temporary or permanent basis accounted for 37% of leavers (2,205), people resigning accounted for 29% (1,740) and retirees 26% (1,545). These proportions have remained relatively stable over the last five years, with the exception of 2020-21, which saw a large rise in voluntary redundancies, therefore reducing the number that may otherwise have resigned.

HMRC has long made use of loans of staff to and from other government departments, particularly HM Treasury, DWP and Home Office. Whilst this can have some benefits for HMRC overall, where there are increasing numbers of staff loaned out and then the loan becomes permanent, it represents a departure for that staff member along with the skills they have developed.

Of those leaving, the average length of service at HMRC amongst those transferring to other areas of the Civil Service is showing a slight downward trend, from an average of 6.2 years in 2020 to 3.74 years in both 2023 and 2024. Amongst those resigning from HMRC, the average length of service has fluctuated, but does show signs of increasing since 2021.

Table 7, Average length of employment at HMRC amongst leavers, in years

It appears that HMRC do not routinely conduct exit interviews when staff leave the department to track the broad reasons for staff leaving. Without this intelligence the departmental management are unlikely to be well equipped to stem the increase in staff leaving by addressing the issues prompting these individual level decisions.

3.1.7. Intention to leave

The annual Civil Service staff survey[12] has long tracked employee intentions over the short to medium term (three years) asking, anonymously, whether the employee had plans to leave the department. In 2019 a staggering 25% of staff responding to the survey reported that they intended to leave HMRC within the next three years. With the impact of Covid-19 this fell to a low of 16.2% in 2021, before partially rebounding up to 18.7% in 2023. The HMRC figures are around the Civil Service mean (20.3%).

It is important to note that the intention to leave always tracks higher than the actual numbers who end up leaving. However, this is of little re-assurance to management as it implies that there are a high number of staff who remain in the department but are unmotivated.

3.1.8. Home working

The survey also asks about whether staff feel they have a choice in deciding where they do their work. Whilst the results for 2023 are encouraging (71.8% of HMRC staff agreed), this was prior to the decision to increase the proportion of working hours spent in the office from 40% to 60% from November 2023. It will be interesting to see how much of an impact this has on next year’s results given anecdotal evidence that its widely disliked.

In Spring 2024 HMRC opened up a significant recruitment for fully qualified tax practitioners who had secured their qualifications whilst working in the private sector, aiming to fill nearly 100 roles. This was intended to complement HMRC staff who had completed their full inspector training under previous schemes. No data has been published about the outcome of this recruitment campaign to date. The mandatory requirement to work 60% of contracted hours from a HMRC office was one of the reasons applicants could give if they wanted to withdraw their candidacy. This implies HMRC management are aware that this inflexibility can be an off-putting factor for individuals considering progressing their career within the department.

3.2. Staff training and development

HMRC offers specific training for staff, the closest equivalent to the Chartered Tax Adviser designation of the CIOT being the Tax Specialist Programme (TSP). Until recently the programme was accredited by Manchester Metropolitan University as equivalent to an undergraduate degree. However, the course is no longer certified, and the length has been shortened from four to three years.

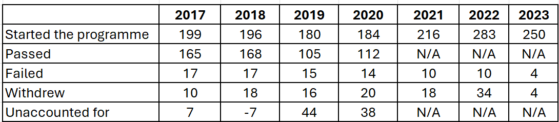

The number of TSP course participants has increased in the last two years. Between 2017 and 2021 the average number of people starting the course was 195, in 2022 the figure increased to 283, and fell somewhat to 250 in 2023.

HMRC are unable to calculate pass rates per cohort as they don’t have the underlying management information, which is concerning as it means they are unable to evaluate the programme effectively. Based on follow up queries they explained that the numbers unaccounted for from earlier years reflect the number of candidates deferring their studies by a year or more (table 8).

Table 8, TSP participation and outcomes

There is concern about HMRC’s ability to retain trained staff as they are often courted by private sector tax advisory firms once qualified, given higher remuneration packages compared to fixed Civil Service pay scales. Of those who passed the TSP, we only have data for how many remain in the department 12 months after completing the programme, but this is quite high (at least 95%). We would need equivalent figures over a longer time horizon to evidence that retention isn’t the problem that anecdotal evidence suggests it may be.

3.3. Staff remuneration

As we have identified earlier, the term ‘tax professional’ at HMRC does not mean someone who is either qualified (either by internal or external qualifications) or experienced in tax work. Indeed, HMRC have recently advertised ‘tax professional’ roles at grade O on a salary of £28,341 outside of London. In last year’s SOTA we identified that ‘tax professionals’ have lower median salaries than other ‘professions’ within HMRC. Recruiting ‘tax professionals’ on lower grades explains this difference.

Comparing median salaries by grade in HMRC with all civil servants (including HMRC) it is clear that across all grades, except for EO, median salaries in HMRC are lower than the Civil Service median. The difference is most significant at SEO/HEO grades with HMRC paying 8% less than the Civil Service median.

Table 9, Median salaries by grade, 2023-24

The reason that the overall median for HMRC is higher than the whole civil service is that HMRC has higher proportion of its workforce in higher grades. This discrepancy may help to explain why so many HMRC staff are transferring to other governmental departments.

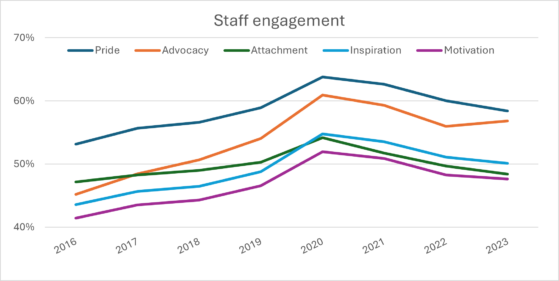

3.4. Staff engagement

The annual staff survey includes measures of ‘staff engagement’, a composite score based on five different elements of engagement with HMRC as a place of work[13]. As in previous years, staff in HMRC report lower levels of engagement than the Civil Service average, scoring 56.4% versus 60.7%. HMRC engagement was down slightly from the previous year (59.1% in 2022). HMRC scores are held down particularly in relation to questions on motivation and attachment to the organisation, both of which averaged below 50%. All measures have declined since 2020, although ‘Advocacy’ showed a small increase in 2023. As this is a snapshot in time (conducted across a five week period in Autumn each year) the survey doesn’t capture the impact of more recent changes to working patterns.

Figure 7, Staff engagement breakdown

In addition to the staff engagement index, the survey also asks about staff satisfaction with pay and benefits[14]. Less than a third of HMRC staff are satisfied with their pay and benefits (30.8%), reflecting below inflation pay awards and several years when pay was frozen in cash terms. This is around the Civil Service mean average of 31.7%.

HMRC staff satisfaction with pay has improved from a low in 2019 when it was just 20%, reflecting a pay award made last year, and one on the cards for Autumn 2024 if the main unions of FDA and PCS accept the offer[15].

There is somewhat better news in relation to perceptions of leadership and managing change, which has long been a major drag anchor on HMRC’s overall engagement score. Almost half (46.3%) reported positive perceptions of leadership and managing change. This is in line with the Civil Service average of 48%.

4. Customer Service

Moving customer interactions onto digital platforms is central to HMRC meeting their customer service plan and delivering £75 million per year in efficiency savings promised at Spending Review 2021. However, in 2023-24 HMRC overspent by £36 million on around 1,000 additional, albeit temporary, customer service staff. Despite this spending, customer service levels have not improved, and in certain areas have deteriorated further.

According to a report by the National Audit Office (NAO) in May 2024[16], HMRC are planning significant staff reductions in customer service in the current year (2024-25) due to budgetary constraints. To do so, it needs to reduce its overall customer service workforce by 14%. As a consequence, HMRC forecast that it would have 950 staff fewer than it needed to meet its performance targets in 2024-25.

Following the NAO report The Treasury announced extra funding of £51 million for HMRC customer service. This followed an admission by Jim Harra, Chief Executive of HMRC, to The Treasury Select Committee, that HMRC did not have the resources to provide the standard of service that customers deserve. The additional funding was designed to provide an extra 1,500 telephone helpline staff, for 2024-25 only. As TaxWatch[17] reported at the time, such short-term measures do not address ingrained problems, such as the lack of properly trained staff, and longer-term strategic planning is required, rather than the occasional sticking plaster.

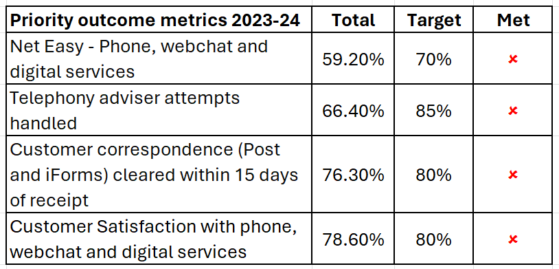

Unsurprisingly, HMRC failed to meet and of its customer service priority outcome metrics for the year.

Table 10, HMRC’s priority outcome metrics

4.1. Volume of communication

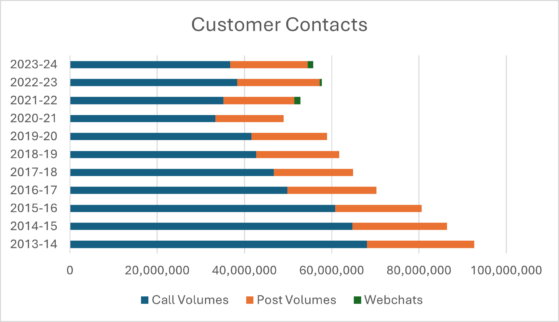

As figure 9 shows, there has been an overall decrease in people attempting to contact HMRC over the last decade, from 92 million contacts in 2013-14 to 55 million in 2023-24, a 40% decrease. Presumably this is largely due to HMRC’s increasing online presence.

HMRC appears to have hit the point at which their current online presence is not equipped to further reduce the need for customers to contact HMRC directly, as many queries are more complicated. This is deeply problematic. The low hanging fruit of simple queries relating to forgotten passwords etc. seems to have been picked. It will be interesting to see whether the much delayed Making Tax Digital can have a significant impact on the overall number of contacts.

Figure 9, Customer contacts

4.2. Telephone

During the year, HMRC either closed or restricted access to a range of phone services to induce people to use their online resources, but also to free up staff to deal with processing backlogs. Three helplines in particular were affected, the Self Assessment, VAT registration and dedicated Agents’. However, the reaction to closures amongst customers was largely negative, with HMRC being forced into a hasty U-turn just 24 hours after announcing it would close the Self Assessment helpline between April and September each year.

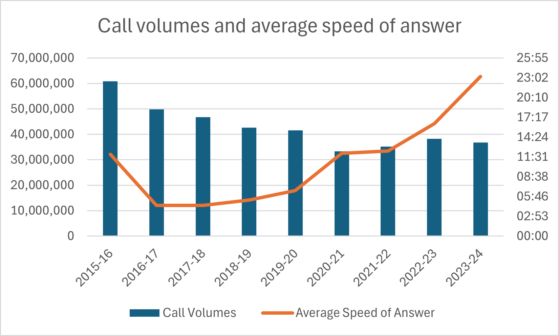

As TaxWatch has repeatedly highlighted throughout the last year, the ability to speak to HMRC on the phone continues to blight taxpayers’ lives and the situation continues to deteriorate. The length of time taken to answer calls is increasing from over 23 minutes in 2023-24, up from 16 minutes in the previous year. This is despite the addition of temporary staff to answer calls.

Figure 10, Call volumes and average speed of answer

As the NAO report[18] released in May 2024 points out, although the number of calls received by HMRC has fallen over time, the amount of time spent by advisers on each call has increased, meaning that the overall workload has not fallen as HMRC had intended and wished for. TaxWatch[19] has also highlighted the use of temporary, low paid contracts for telephony operators, with minimal training provided to those dealing with potentially complex tax cases as a contributory factor in poor levels of service.

These figures do not take into account the time spent by those who abandoned calls or were cut off. Whilst the percentage of calls handled was 77.4% for the year 2023-24, an increase from the previous year, this still leaves a significant number of callers unable to speak with an advisor. In total over 8 million calls were not handled during the year. This inevitably impacts on voluntary compliance and error rates, if taxpayers are unable to speak to an advisor about their tax issues.

Call volumes vary throughout the year, with spikes around the self-assessment deadline of 31 January and the end of the tax year. In October 2023, HM Revenue and Customs (HMRC) announced a pilot for a new working arrangement, offering 100 customer service staff working longer hours in the winter and shorter hours in the summer under an ‘annualised hours’ scheme for a small overall pay increase. It will be interesting to see whether the pilot has a positive impact on customer service levels as hoped and thus extended to more staff.

4.2.1. Talking to a human

Calls to HMRC are screened by automated messages aimed at redirecting them to other options e.g. submitting a webform, rather than remaining on the line to speak with an adviser. In 2023-24 the percentage of callers staying online to speak with an adviser had fallen to 66.2% (down from 76.5% in 2021-22), exacerbated by a new policy for the 6 weeks leading up to the Self-Assessment deadline for the 2022/23 tax year of 31 January 2024 which cut off callers whose queries did not relate to the Self-Assessment deadline or could be dealt with via the webform.

4.2.2. Customer satisfaction

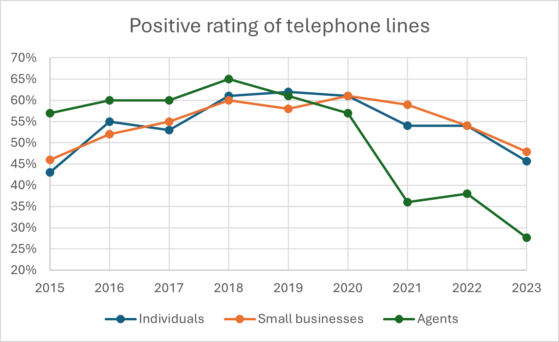

Unsurprisingly, customer satisfaction with HMRC telephone lines has decreased in recent years. An annual survey[20] conducted on behalf of HMRC measures ratings of HMRC telephone lines[21] amongst three different taxpayer sectors, individuals, small businesses and agents. Since 2018 the percentage of agents with a positive rating of HMRC’s telephone lines has collapsed, from 65% to below 30% in 2023 (figure 11). This should be particularly concerning for HMRC as agents working for multiple clients are likely to spend far more time contacting HMRC than individuals or businesses and will have more complex queries. Members of professional bodies, such as the Chartered Institute of Taxation (CIOT) have become more vocal around this issue as their members express increasing levels of frustration with HMRC’s customer service provision. In giving evidence to The Public Accounts Committee, CIOT stated that customer service levels were the “single greatest concern expressed by its members, and that they are having a detrimental impact on cash flow, the costs of doing business, attitudes to tax compliance and trust in the tax system”.[22]

In response to criticism, HMRC have made changes to the Self Assessment and PAYE helplines for agents, which are being combined into a single helpline. However, HMRC are limiting the number of clients affairs that can be discussed to a maximum of 5 per call. They are also introducing a webchat service solely for agents and new options on the helpline for chasing client re-payments, which HMRC estimate accounted for over a third of calls to the agent dedicated helplines last year[23].

Figure 11, Positive rating of telephone lines

4.3. Webchat

In contrast to phone services, webchat handling rates remained high, at 95.9% of submitted webchats being handled by advisors. However, the number of webchats are lower in volume than telephone calls, with just 1.3 million in 2023-24, compared to the 36.7 million telephone calls.

There’s also a stark difference in overall customer satisfaction levels; 74.5% satisfaction rating for webchats and 42.9% satisfaction level for telephone[24]. Webchat queries are predominately on more straightforward matters compared to the residual cases progressing through the telephone lines.

4.4. Post

Although the number of telephone calls HMRC receives has fallen dramatically over time, the volume of postal correspondence remains relatively stable, falling by only 10% since 2015-16.

![]()

Figure 12, Post volumes and percentage cleared

Three quarters of post and iForms are cleared within 15 working days[25], and almost 90% cleared within 40 days. However, this leaves 10% still not dealt with after 40 days. As we reported in SOTA 2023, once a piece of post is more than 40 days old, dealing with it will no longer contribute to meeting HMRC targets, disincentivising dealing with it. In response HMRC set up a taskforce to deal with post that was more than 12 months old. The taskforce is still ongoing[26].

4.5. Online Personal and Business Tax Accounts

Despite a large rise in the number of people accessing them, totalling 199 million hits in 2023-24 (compared to 66 million in 2016-17), overall use and awareness of online Personal and Business Tax Accounts remains relatively low, albeit growing from a small base. In the latest survey only 34% of individual respondents reported having a Personal Tax Account, 13% had heard of them but did not have one, and over half of respondents (53%) had never heard of them. HMRC have been marketing the features of tax accounts, for example to people in the queue to speak to an advisor. However, to increase take up further, the accounts require greater functionality to take on more of the customer service queries which are currently dealt with over the phone.

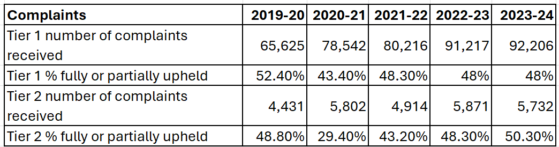

4.6. Complaints

HMRC operates a formal two-tier complaints process. Tier 1 is HMRC’s first attempt to resolve a complaint. If the complainant is not satisfied with Tier 1 response, they can ask that the complaint be investigated again, progressing to a Tier 2 complaint.

The number of Tier 1 complaints received has climbed consistently over the last five years, reaching a historic high of 92,206 in 2023-24. However, the proportion of complaints either fully or partially upheld has shown some signs of decreasing in recent years. HMRC do not provide data on the nature of complaints made, so we cannot make any assertions about what is driving the increase. We can only surmise that the increase is related, at least in part, to its poor customer service performance.

Table 11, Complaints received and upheld

5. Compliance

Compliance refers to activities undertaken by HMRC to ensure that taxpayers adhere to tax laws and regulations, encompassing activities aimed at reducing the tax gap by ensuring accurate reporting, timely payment of taxes, and effective enforcement against non-compliance.

HMRC’s compliance activities can be broadly split into two areas, ‘downstream’ and ‘upstream’. Downstream compliance activity relates to interventions made by HMRC into actions and behaviour that have already taken place – focussing on identifying past non-compliance, e.g. fraudulent or erroneous claims for relief that emerge through enquiries into tax returns. Part of the yield is the estimated impact of this activity on the future behaviour of the taxpayer.

Upstream compliance activity relates to the prevention of non-compliance before it happens, based on the estimated impact of legislative changes to close tax loopholes and changes to internal HMRC processes, to reduce opportunities to avoid or evade tax. It also includes an estimate of the impact of activities undertaken to educate taxpayers, as well as ‘nudge’ campaigns, including ‘one-to-many’ letters sent to UK resident individuals who have offshore bank accounts, but may not have included offshore income and gains in their tax returns. It is harder to quantify yield estimates accurately because there’s a lack of a ‘counterfactual’ against which to measure.

5.1. Compliance checks

Whilst the number of compliance checks undertaken by HMRC in 2023-24 has increased from the previous year, the number remains lower than the pre-COVID figures. That being said, both those opened and closed in 2023-24 exceeded 300,000 for the first time since before the pandemic. It is also the first time in over five years that the rate of closing checks outpaced those that were opened.

Table 12, Compliance checks opened and closed

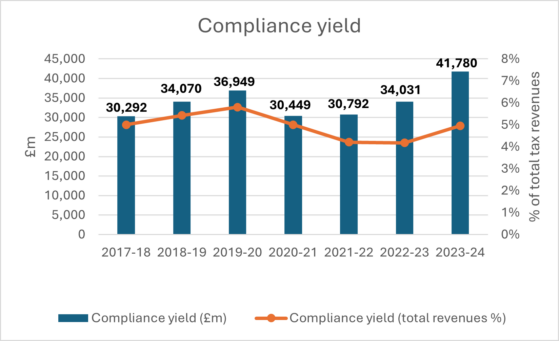

5.2. Compliance yield

The compliance yield is an estimate of the revenues that would have been lost but for HMRC’s compliance activities as well as the impacts of policy changes designed to reduce non-compliance.

The proportion of the total compliance yield attributed to downstream activity has dropped significantly over time, from 77% in 2019-20 to 67% in 2023-24, but yearly figures can be skewed by sizable individual cases, such as the Bernie Ecclestone case (see below) that concluded during the 2023-24 tax year. It’s a broad HMRC estimation of its own efforts to prevent non-compliance before it happens.

In 2023-24 the increase in the upstream compliance yield was driven by the doubling of the estimate for ‘Upstream operational yield’, which measures, amongst other things, the deterrent effect of “securing certainty of tax treatment at litigation”[27], the meaning of which is unclear to TaxWatch.

The total compliance yield increased by 22.7% from the previous year, from £3.4 billion in 2022-23 to £4.1 billion in 2023-24, exceeding HMRC’s compliance target by £1.28 million for the first time since 2019-20. However, HMRC cannot rely on such sizable cases each year to meet its compliance targets.

Table 13, Tax compliance yields

Note: *Compliance targets were suspended in 2020-21 and 2021-22 due to the COVID pandemic, as many staff were transferred to help with compliance into HMRC administered support programmes such as the job retention scheme known colloquially as ‘furlough’.

Figure 13, Compliance yields and total revenues

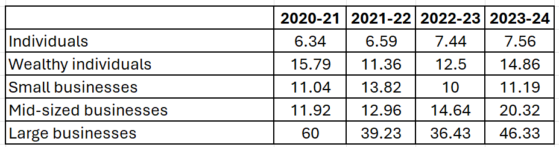

5.3. Return on investment (‘ROI’)

The return on investment from compliance activities is a ratio calculated for every £1 spent on compliance activities compared to the amount collected in revenue yield. The return on investment in HMRC compliance has been historically high and continues to be so in 2023-24. The overall return on investment in the year was 17.5, however, the figure varies depending on customer group. Large businesses produce the most valuable returns and are increasing again after two years of decreasing. Yields amongst small businesses have also increased, whilst those for individuals and wealthy individuals, have remained constant in recent years. The persistence of good returns on investment is a strong argument for making more resources available to HMRC to continue to improve the overall compliance yield.

Table 14, Return on investment per customer group

5.4. Tax disputes

If HMRC and a taxpayer disagree over a tax liability there are a number of means of settling tax disputes.

5.4.1. Statutory reviews

A taxpayer can challenge a decision made by HMRC by requesting a statutory review of the decision, a quicker and more cost effective option, before potentially embarking on a direct appeal to tribunal.

The vast majority of statutory reviews (90.7%, 50,881 of 56,107 in 2023-24) related to automated penalties and default surcharges. However, the proportion of automated penalty and surcharge decisions made by HMRC upheld at statutory review was dramatically lower (26%) than the rate of all other reviews (71.4%) which suggests there is a real problem with the accuracy of the automated penalty system that should be addressed.

5.4.2. Alternative Dispute Resolution (ADR)

ADR is a form of mediation and is used mostly where the taxpayer has appealed against a formal HMRC decision. It is only available to taxpayers in certain circumstances, and as such is not widely used. In 2023-24, there were only 1,309 applications for ADR, of which 512 were accepted. However, ADR does have a high resolution rate. Of the 367 cases closed in 2023-24, 307 (83.7%) were resolved, meaning that agreement was reached between HMRC and the taxpayer. The benefit of ADR is that it avoids the cost of going to Tribunal in a case. Cases that aren’t eligible for ADR or whose application is not accepted are where there are hallmarks of dishonest conduct by the taxpayer, or instances where there may be other taxpayers in similar situations and HMRC may wish to establish a “test case”.

5.4.3. Tribunals

Although most appeals are settled between the customer and HMRC without requiring the tribunal or court (e.g. ADR or statutory review discussed above), a significant number do make it to tribunal each year, and the first stage is the First Tier Tribunal (FTT). If HMRC or the taxpayer disagrees with the decision of the FTT, a further appeal might be able to be made at the Upper Tribunal[28], then the High Court, Court of Appeal and ultimately, the Supreme Court.

12,668 new appeals were made to FTT during 2023-24 and at the end of the year, there were 47,250 appeals in progress, the majority of which (41,750) have been ‘stood over’, which generally means that HMRC and the customer have agreed to put the appeal on hold while waiting for a decision in a related lead case is being litigated. The number of remaining appeals in progress was bizarrely the same as in 2022-23, at 5,500, suggesting that the backlog in cases, whilst not improving, is not worsening.

A total of 7,885 cases were decided either by formal hearing or agreement prior to the hearing during 2023-24, yielding £3.3 billion. The success rate for HMRC in decided appeals remains high, at 87.4% in 2023/24, which is consistent with previous years.

5.5. Fraud Investigation Service

HMRC’s Fraud Investigation Service (FIS) deals with the largest and most complex compliance enquiries. It has both civil and criminal powers to conduct and prosecute investigations, although its stated policy is to make most frequent use of civil powers to deal with fraud, as the most cost effective means of recovering lost tax revenues. Criminal investigations are reserved for cases where either HMRC wants to send a strong deterrent message to others who might consider such behaviour, or where HMRC views that a criminal sanction is appropriate.

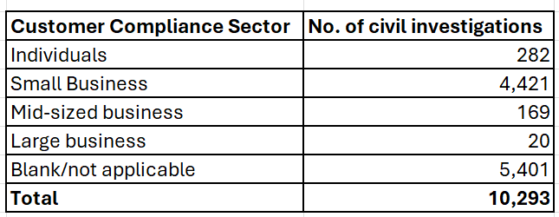

HMRC’s Annual Report states that there were over 10,200 civil investigations into suspected fraud, opened by FIS, during 2023-24. TaxWatch submitted a Freedom of Information request to obtain a breakdown of the nature of these investigations, based on customer compliance sector and by tax. HMRC advised us that they do not always record the customer compliance sector of the subject of investigations, so there is missing data for more than half of cases (which is a source of worry in terms of HMRC’s management systems tracking cases and spotting patterns). However, what data is provided suggests that most civil fraud cases relate to small businesses, which account for 43% of all investigations.

Table 15, Investigations by taxpayer

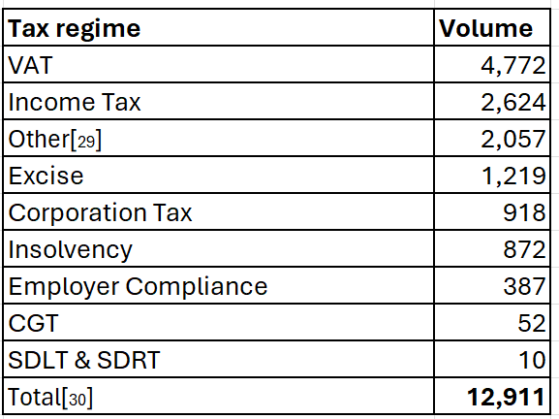

The types of tax subject to fraud investigations reflects the customer compliance sector focus on small businesses, with the majority of investigations relating to either VAT or income tax.

Table 16, Investigations by tax regime

5.5.1. Criminal cases

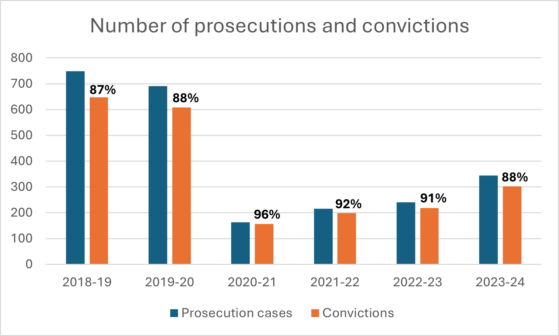

The number criminal prosecutions in 2023-24 increased from the previous year but remains far below the number of prosecutions undertaken prior to the COVID pandemic. The year-on-year increase suggests that HMRC is moving slowly in the right direction to re-establishing a message of deterrence to those who might be tempted to undertake fraudulent behaviour. However, they are failing to use the full extent of their powers to bring criminals to justice, undermining the deterrent effect.

Figure 14, Prosecutions and convictions

The number of positive charging decisions (i.e. cases where the Crown Prosecution Service authorises the charging of an individual) has increased since last year. In 2023-24, there were 501 positive charging decisions, compared to 433 in 2022-23. However, as we reported in last year’s SOTA[29], if these figures are compared with the number of cases reaching the courts, 344 in 2023-24, this suggests that the number of cases waiting for court time is increasing. This demonstrates delays in other parts of the public sector are affecting HMRC’s ability to pursue the necessary deterrent effect of (timely) convictions for tax fraud.

5.5.2. Civil cases

FIS carries out civil enquiries using two Codes of Practice, 8 (CoP8) and 9 (CoP9). CoP8 is used where fraud is not suspected at the outset of the investigation, but HMRC believe that large amounts of tax are owed due to the use of complex tax arrangements or avoidance schemes. If fraud is suspected at the outset CoP9 is used, and if a case starts under CoP8 but then fraud is uncovered as the investigation unfolds, a CoP8 case can be converted into a CoP9 investigation, which is a more structured process.

Although CoP9 is reserved for cases where HMRC suspect tax fraud, it remains a civil, rather than criminal investigation. CoP9 provides the taxpayer with the opportunity to make a full disclosure, normally through the Contractual Disclosure Facility (CDF). If the taxpayer does this, HMRC will not open a criminal investigation, despite the suspected presence of fraudulent behaviour.

The Bernie Ecclestone Case

The Bernie Ecclestone case, decided in October 2023, is a good example of the civil and criminal powers available to HMRC and the potential consequences of failing to make a full disclosure. It also highlights the length of time, and considerable resources required, to undertake and complete a criminal investigation.

Bernie Ecclestone was given a suspended custodial sentence, in addition to being ordered to pay a total of over £650m in relation to tax, interest and penalties, after pleading guilty to a charge of fraud by misrepresentation after telling HMRC that he was not connected to any offshore trusts, other than a single trust set up for his children, which was untrue.

The investigation began in 2012, as a CoP8. However, information uncovered during the investigation lead HMRC to open a CoP9 investigation, at which point Ecclestone was given the opportunity to make a full disclosure, which he failed to do. This failure lead in turn to a criminal investigation, which resulted in the prosecution of Ecclestone and his guilty plea.

The case was a success for HMRC, which they view as having a significant deterrent effect, but highlights the time and resources required to undertake complex enquiries.

5.5.2.1. CoP8

The number of CoP8 cases closed in 2023-24 dropped sharply compared to the previous year. However, both the total and average yields increased, with the average yield doubling, indicating that the closed cases were of higher value than those in previous years. The significant decrease in new cases may reflect HMRC’s focus on targeting those with greater potential value.

Table 17, CoP8 cases

5.5.2.2. CoP9

In July 2023 HMRC issued a revised policy booklet for CoP9, designed to ensure a more robust approach to cases where fraud is suspected as the “ultimate civil compliance tool” available. It is therefore surprising to see the number of CoP9 cases both opened and closed in 2023-24 fall compared to the prior year. Although the yield recorded increased from £89m in 2022-23 to £991m in 2023-24, this is an anomalous year, due to the inclusion of particularly large settlement reached during the year, which accounts for a large proportion of the total yield.

Table 18, CoP9 cases

Whilst these figures suggest that HMRC are focusing more on cases with higher potential value, such an approach may undermine the overall efforts to deter fraudulent behaviour, for more numerous, individually lower value, activities, safe in the knowledge that HMRC is focused on bigger fish.

5.6. HMRC’s failure to use its powers

As reported in last year’s SOTA, criminal prosecution is an important element of HMRC’s powers for tackling serious offences, creating a deterrent effect. However, as TaxWatch and other commentators and tax professionals have repeatedly argued, a deterrent is not a deterrent if it is not used. HMRC are not using the full extent of their powers to impose penalties, nor prosecuting cases where there is a criminal charge on the statute book.

One example, amongst many, is the failure of HMRC to use the power to sanction persistently uncooperative behaviour, which was given to HMRC in Finance Act 2016. A freedom of information request reveals that HMRC have never used this power, despite stating that it was designed to act as a “deterrent to the small number of large businesses who persistently engage in aggressive tax planning and/or refuse to engage with HMRC in an open and collaborative way”.[30]

5.7. HMRC ‘bloopers’

In addition to failing to use the full extent of its powers, there have been recent stories covering seemingly simple and unforced errors made by HMRC officials which have resulted in them losing tribunal cases, costing millions in lost tax revenues.

One such case was decided in September 2024. The First Tier Tribunal ruled in favour of the taxpayer appealing a tax ruling made by HMRC that he owed income tax on incorrectly claimed business expenses as an employee. The taxpayer had engaged the services of an accountancy firm, Apostle Accounting Ltd, which is currently subject to criminal investigations, and many of whose clients have been sent letters by HMRC demanding the repayment of tax for erroneous claims. However, HMRC lost the case as the HMRC officer responsible for the case failed to turn up to the Tribunal to give evidence[31].

The most egregious error relates to procedural mistakes made in imposing a £14 million penalty on a taxpayer whose tax avoidance schemes HMRC estimate to have cost the Treasury £1 billion in lost taxes[32].

These errors suggest that HMRC lacks sufficient experienced staff to ensure the correct procedures prior to and during Tribunal proceedings are followed. The result is wasted time and lost tax revenues and undermines confidence within the workforce.

6. Conclusion

During a period when public finances are under pressure and tax is taking centre stage in addressing the dire financial situation, HMRC is struggling under the weight of expectation. As the report highlights, it lacks the resources required to effectively undertake and fulfil its role as administrator and collector of taxes.

The issues identified in the report cannot be solved by short term injections of cash to stave off the worst effects of underinvestment. Instead, a long term considered approach to how HMRC functions in a more nimble and efficient way to cope with an increasingly complex tax code and within competing demands, is required.

Notes

[1] Summary Statistics – GOV.UK (www.gov.uk)

[2] Are we nearly there yet? In search of the elusive offshore tax gap – TaxWatch (taxwatchuk.org)

[3] Spring Budget 2024 (HTML) – GOV.UK (www.gov.uk) table 5.1, measure 26

[4] It can be difficult to fully reconcile the staff figures at HMRC due to differences in counting methods. HMRC statistics are a mix of ‘full-time equivalent’ (FTE) and actual numbers of staff; ‘headcount’. Where staff figures are used they are identified as either FTE or headcount.

[5] These figures are HMRC core department and exclude those working in the (separate) Valuation Office Agency. Staff who had been within Revenue and Customs Digital Technology Services Ltd have been brought back into the core department by 2023/24.

[6] The number in the main directorates does not sum to the total number of staff as some staff do not work in the three main directorates.

[7] Hanging on the telephone: The front line of HMRC’s customer service? – TaxWatch (taxwatchuk.org)

[8] Will £51m really fix HMRC’s customer service helpline? – TaxWatch (taxwatchuk.org)

[9] whitehall-monitor-2024_0.pdf (instituteforgovernment.org.uk), p42

[10] Staff turnover is calculated based on the number of employees who left divided by the average number of staff. Turnover excludes VOA.

[11] whitehall-monitor-2024_0.pdf (instituteforgovernment.org.uk), p18

[12] The overall response rate to the survey across the Civil Service was 65%, so there are questions over how representative of the whole Civil Service the averaged results are.

[13] The five questions are: I am proud when I tell others I am part of [my organisation]; I would recommend [my organisation] as a great place to work; I feel a strong personal attachment to [my organisation]; [My organisation] inspires me to do the best in my job; [My organisation] motivates me to help it achieve its objectives. Responses to each statement are in the form of scales of agree to disagree. The engagement scale is based on the proportion of respondents who either ‘Strongly agree’ or ‘Agree’ with the statement.

[14] Pay and benefits theme score is based on three questions, with agree-disagree scale responses: I feel that my pay adequately reflects my performance; I am satisfied with the total benefits package; Compared to people doing a similar job in other organisations I feel my pay is reasonable.

[15] Starmer plays down prospect of above-inflation public sector pay deals (civilserviceworld.com)

[16] HMRC customer service – NAO report

[17] Will £51m really fix HMRC’s customer service helpline? – TaxWatch (taxwatchuk.org)

[18] HMRC customer service – NAO report

[19] Will £51m really fix HMRC’s customer service helpline? – TaxWatch (taxwatchuk.org)

[20] Individuals, Small Businesses and Agents Customer Survey 2023 – GOV.UK (www.gov.uk)

[21] The responses range from Very good (5) to Very poor (1). Positive responses count those who responded either 5 or 4.

[22] Public Accounts Committee – HMRC customer service at record low (tax.org.uk)

[23] Changes to the Agent Dedicated Line from 7 October 2024 (tax.org.uk)

[24] The breakdown of satisfaction levels for phone and webchat are new for 2023-24.

[25] From 2021-22 the percentage includes both post and iForms. Prior to this they only include post.

[26] HMRC extends trial for responding to old post | ICAEW

[27] HMRC compliance yield: technical note – GOV.UK (www.gov.uk)

[28] Although not all cases can be appealed to higher courts.

[29] State of Tax Administration 2023 – TaxWatch (taxwatchuk.org)

[30] FOI request made to HMRC by TaxWatch.

[31] Julian Lowe v The Commissioners for HMRC – Find Case Law – The National Archives

[32] HMRC errors let a notorious tax avoider escape a £14m penalty (taxpolicy.org.uk)