- Nearly £40bn of tax revenues go uncollected in 2022-23 – £4bn more than prior year

- Non-compliance estimated at 4.8% of all tax owed. 2021-22’s percentage has been revised up from 4.8% to 5.2%

- Major reasons for the jump are:

-

- Behaviours: Higher non-payment/tax debt, now 13% of the gap

- Taxes: Corporation Tax making up a greater than ever proportion (34%, double that in 2018-19) vs other major taxes where the gap proportion is flat or falling

- Taxpayer type: small businesses continue to dominate – making up 60% of the overall figures

- Inflation and fiscal drag increasing tax as a proportion of the UK’s economy, so whilst the proportionate tax gap is flat, greater absolute amounts are lost.

-

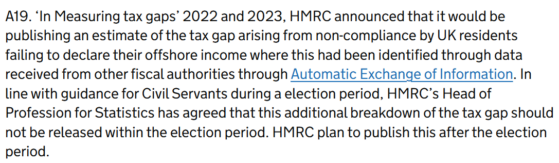

- Offshore tax gap, originally due 12 months ago has been further delayed – HMRC say that they plan to publish this after the UK’s General Election. This suggests the offshore tax gap is larger than currently acknowledged and thus politically sensitive.

The Tax Gap is defined as “the difference between the amounts of tax that should, in theory, be collected by HMRC, against what is actually collected”. This is a broad measure of tax non-compliance, which covers tax losses arising for a variety of reasons – from innocent mistakes to complex frauds carried out by criminal gangs.

HMRC has been collecting data and making estimates of the Tax Gap since the early 2000s, and has published them every year since 2008. There have been numerous revisions to past Tax Gap estimates, which make some year to year comparisons complicated but the methodological approach is broadly similar over time.

We dive into some of the interesting trends below.

Points of interest

Small businesses are responsible for the largest proportion of the overall tax gap – now 60% compared to other categories of taxpayer (HMRC use the quaint term ‘customer segments’). Their share has been consistently increasing over the last few years, from a low of 38% in 2016-17.

The main tax area accounting for most of the problem is corporation tax, where small businesses have had a tax gap of over 30% for the last four years – up from 11% in 2011. No other major tax type has seen an increase in its tax gap figure of anything like these amounts, with more accurate estimates of fraud and error within the Research & Development Tax credit regime a particular factor, discussed here.

Last year, HMRC committed to publishing figures for the “offshore” tax gap during 2023, but then this was delayed twice, and was due to be included within today’s report following a random enquiry programme based on automatic exchange of information data HMRC receives data about assets owned by UK taxpayers in other countries. This has been delayed yet again, with a minor note hidden within the methodological annex implying that the release could be viewed as politically contentious:

TaxWatch continues to press for scrutiny of this vital component given upcoming changes to the taxation of UK residents some of whom will be affected by the upcoming changes to the non UK domiciled regime.

Individuals classed by HMRC as wealthy – which covers around 850,000 people (defined as those with incomes of £200,000 or more, or assets equal to or above £2 million in any of the last 3 years) – are responsible for around 5% of the tax gap, equal to the tax gap for all other individuals combined (numbering 34 million within PAYE and 7 million within self -assessment). While wealthy taxpayers are dealt with by specialist teams and have a greater level of scrutiny, we would expect these taxpayers to have assets held overseas, so until the offshore tax gap is made public we can assume that this is an underestimate and that more resources should be focussed on compliance to recover lost revenues.

Error and carelessness account for 45% of the tax gap, indicating that other, more serious, behaviours are involved for over 50% of the gap – a sum of over £22bn. Non-payment has jumped by nearly £2bn to £5.5bn, now comprising 13% of the overall tax gap, up from 8% just last year. With the end of Time To Pay arrangements for taxpayers struggling with cashflow during the Covid-19 pandemic, more of these debts being assessed as irrecoverable through personal and corporate insolvency action.

NB/ Fraud and error arising in the Covid schemes no longer forms part of the tax gap reporting, following the publication of a standalone analysis of the schemes for the period for which they operated (2020-21 and 2021-22) here.

The absolute amounts lost to evasion (£5.5bn, or 14%) and avoidance (£1.8bn or 5%) are higher than previous years but represent mainly fiscal drag and inflation meaning the sums involved in estimated avoidance and evasion are structurally larger than in prior years.

We would note that in the coming General Election the three main parties all are promising to deliver greater revenues from closing the tax gap over the course of the next Parliament especially in relation to evasion and avoidance – that this is much easier said than done. Without significantly more resources deployed smartly the absolute tax gap will continue to increase, if not undoing the progress on the relative tax gap made in recent years.