- HMRC accounts qualified again due to persistent large scale error and fraud in SME R&D scheme

- Levels of error and fraud falling, but remain a material issue for HMRC

- HMRC needs to address compliance without disincentivising legitimate claims

- Tax Reliefs need to design non-compliance out from the beginning

As part of the larger story around closing the tax gap a significant amount of attention has recently been paid to the losses to fraud and error within the Research and Development tax relief scheme for small and medium sized companies (SME R&D tax relief), with new data within HMRC’s Annual Report & Accounts 2023-24.

Once again, the National Audit Office qualified HMRC’s accounts due to a “material level of error and fraud in Corporation Tax research and development reliefs”. The good news is that the estimated error rate within the relief is coming down from the previous high of 25% of all claims, or £1.2bn, in 2021-22. But the new estimate remains unacceptably high at 14.6%, or nearly £0.5bn. It has taken years for HMRC to admit there were problems (despite plenty of commentors including TaxWatch sounding the alarm), and action has been too slow to avoid the situation getting totally out of hand.

A stitch in time saves nine…

The relief, introduced in 2000 has become synonymous with inaccuracy and abuse – and many of the problems were foreseeable from the design which, allowed to fester, has required huge amounts of resources, invested in compliance and customer education, with numerous changes to the scheme aimed at reducing levels of error and fraud. The National Audit Office, reporting on the accounts, described the abuse of the scheme as “among the highest reported across all government spending programme, including those administered in response to the COVID-19 pandemic”.

The accounts have once again been qualified suggesting that it remains a significant and ongoing issue for HMRC. Due to the proliferation of error and fraud in the scheme, a bulk compliance effort has been required, threatening the integrity of the scheme from the other end of the spectrum, with many valid claims being denied. Despite the efforts made by HMRC, the auditor concludes in the 2024 report that:

“(the) impact of the actions HMRC is taking to tackle abuse of Corporation Tax research and development reliefs will not become clear until 2024-25 and beyond, when the legislative changes and improvements to its compliance processes take effect and HMRC has conducted an evaluation of the impact of these changes. Given what HMRC now knows about the extent of non-compliance in the schemes, it will need to consider whether the steps it is currently taking are adequate and whether it is striking the right balance with its compliance interventions, to avoid deterring valid claims.”

As TaxWatch has previously written, the SME R&D tax relief scheme has been open to abuse and error for many years and, despite the efforts of government and HMRC to address the high levels of error and fraud, it remains a significant issue draining tax revenues and HMRC resources in tackling its shortcomings.

Increasing the scope and generosity, increasing the scope for error and fraud

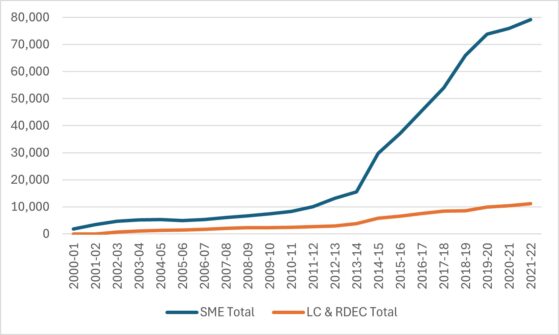

Since its introduction in 2000, the SME R&D tax relief scheme has broadened in scope and increased in generosity, with numerous changes to the nature of qualifying companies and expenditure as well as improved rates of tax relief and credits to be claimed. It is common for tax reliefs to be tweaked following their introduction. Changes invariably make them more accessible and generous. This inevitably results in more claims being made and more lost tax revenues. It also means that tax reliefs become more vulnerable to misuse. R&D tax relief is a good example of this as claim numbers have sky-rocketed over the last 10 years, from 15,585 in 2013-14 to 79,205 in 2021-22 (figure 1). The consequent cost in terms of lost tax revenues has also risen exponentially, with the relief costing £4.76bn in 2021-22, an overall cash increase of 575% since 2013-14[1]. Whilst the number of claims from large companies (LC & RDEC) has also increased, the rate of increase is far lower.

Figure 1. Number of claims for R&D tax credits (source: Corporate tax: Research and Development Tax Credits – GOV.UK (www.gov.uk))

Error or Fraud?

The overall split between error and fraud in SME R&D claims is unknown. HMRC have stated that they found fraud indicators in fewer than 10% of claims examined in the latest random enquiry programme, and these claims accounted for around 5% of the total value claimed[2]. They conclude that the majority of non-compliance is due to behaviours other than fraud.

However, evidence from whistleblowers and others investigating the R&D tax relief scheme, including a report by the House of Lords Economic Affairs Committee, found evidence of large scale organised criminal attacks on the scheme as well as activities of rogue advisers, targeting small companies, persuading them to make invalid claims. TaxWatch therefore questions the validity of the 10% figure cited by HMRC, given the apparent scale of the R&D advisory industry, this appears to be far lower than we would expect. It is also difficult to reconcile recent changes in the scheme with a such a large reduction in losses, with more than a 60% reduction in just two years. Such a large reduction in ‘errors’ would surely take much more time to filter through, given the need to educate such a large number of claimants.

Plugging the leaks

Since 2019, a raft of policy and operational measures have been introduced to plug the leaks of tax revenues. HMRC estimate that policy and operational measures have reduced error and fraud in 2023/24 to 14.6% for the SME scheme, down from 19.5% in 2022/23. However, there are concerns that HMRC’s reaction to the level of error and fraud has led to an uneven approach to R&D tax compliance resulting in many legitimate claims being denied relief and there is a danger that HMRC may undermine the scheme by disincentivising its use by legitimate claimants.

The Economic Affairs Committee report on the R&D tax relief scheme raised significant concerns about HMRCs approach to enquiries, with those in industry claiming a lack of understanding of the complexities and technical nature of R&D claims amongst HMRC staff. This is highlighted by a recent First Tier Tribunal (FTT) case lost by HMRC, which hinged on whether software development amounted to an innovation.

FTT decision – Get Onboard Limited v HMRC

In a decision announced in July, HMRC lost a case against a company claiming R&D tax credits for work done, somewhat ironically, on developing an automated artificial intelligence analysis process for identifying potential fraud through know-your-client (KYC) verification and risk profiling processes. HMRC had argued that the development did not constitute R&D, although provided no rationale for their decision, beyond the view offered by their Chief Digital Information Officers. However, the FTT found that the expenditure did qualify for R&D tax credits, based on the comprehensive evidence put forward by the company. The FTT ruled that there was a shift in the evidential burden back to HMRC to demonstrate why the expenditure did not qualify, in response to the evidence provided by the company. However, HMRC was unable to put forward any such evidence.

The case highlights the technical nature of R&D across a number of specialist domains and the difficult balancing act faced by HMRC in reducing large scale error and fraud in the SME R&D tax credit system, whilst not disincentivising legitimate claims for innovation.

Conclusion

The SME R&D tax relief scheme is a prime example of how tax reliefs are introduced, augmented, misused and abused in the absence of clear strategic thinking on their design and implementation, resulting in large financial losses, due to error and fraud, as well as sucking up huge additional resources in addressing the problems (also called closing the barn door after the horse has bolted).

It is a salutary lesson to policymakers that, to the greatest extent possible, non-compliance should be designed out of tax reliefs before it happens. An example of these failures was allowing tax credit payments to be made directly to agents acting on behalf of claimant companies, rather than the companies themselves, which seemed to be asking for trouble. Yet this was not closed down until an announcement in Autumn Statement 2023.

When designing future tax reliefs, two of the main questions should be;

- How could this be exploited to make fraudulent claims?

- How could claimants get it wrong?

Answers to both questions should be fundamental to any design of future tax reliefs.

More broadly, the problems with the scheme highlight that using non-tax concepts to determine tax credits is always a risky business, open to abuse. The very nature of research and development means that it is a fairly subjective term, requiring detailed knowledge of areas that is clearly beyond what HMRC officers currently have. A lack of domain expertise across HMRC to deal with claims will inevitably result in fraudulent claims being allowed and legitimate ones being denied.

As the FTT decision made clear, it is vital that HMRC develop specialist knowledge, or bring in external experts, to deal with claims effectively. It must also ensure that claimants can engage constructively with HMRC throughout the claims process to ensure compliance without disincentivising valid claims, which would impact negatively on innovation in the UK.

Whilst there is positive news on the estimated amount of error and fraud in the SME R&D tax credit scheme, the full impact of HMRC’s actions to combat this have yet to be understood. What remains clear is that the R&D tax credit debacle is a good lesson in how not to implement a tax relief scheme.

[1] Summary-Tax-measures-to-encourage-economic-growth.pdf (nao.org.uk)

[2] HMRC_annual_report_and_accounts_2023_to_2024.pdf (publishing.service.gov.uk), p.22.